TL;DR:

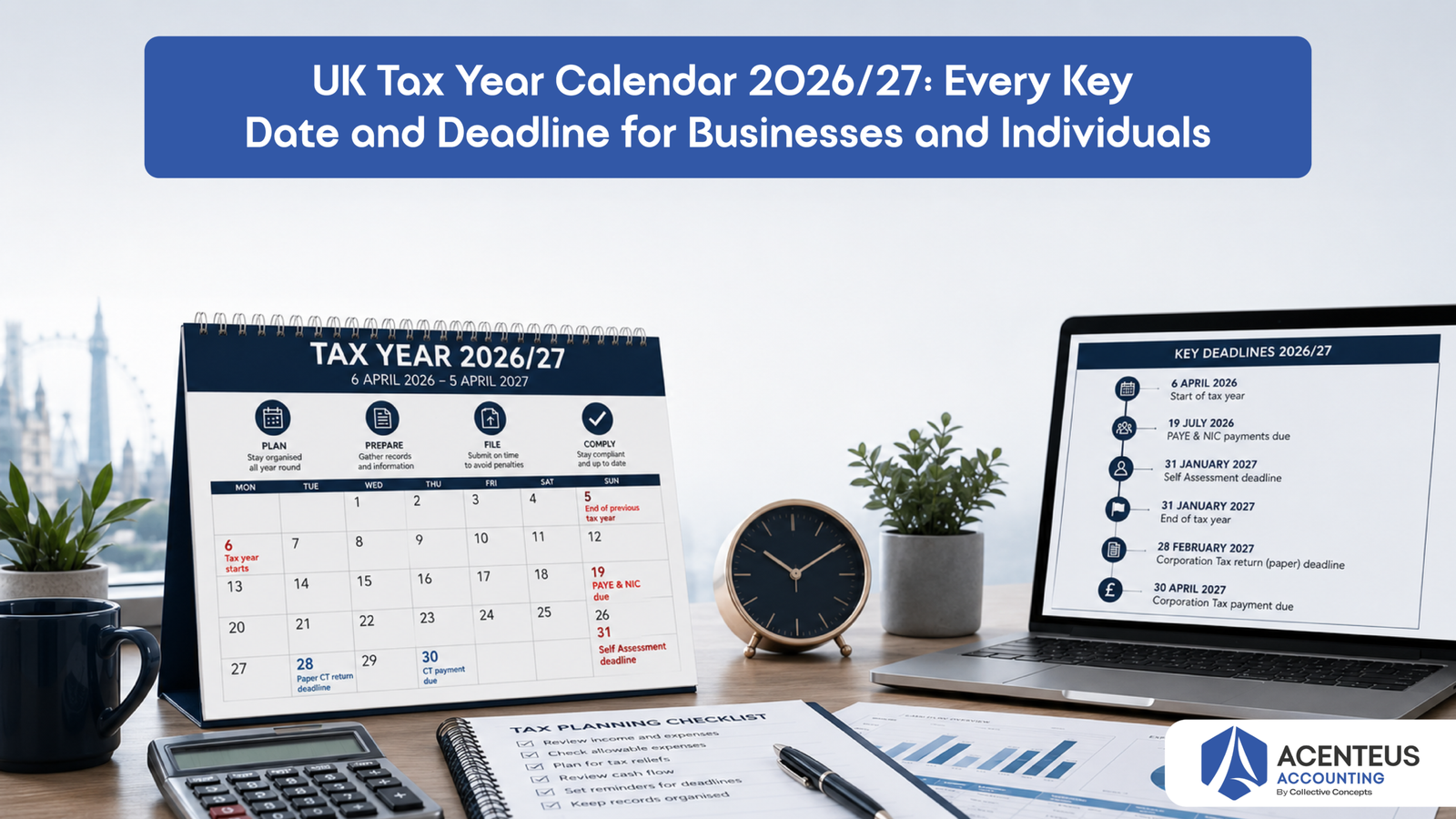

- The 2026/27 tax year runs from 6 April 2026 to 5 April 2027.

- The online Self Assessment tax return deadline and balancing payment are both due on 31 January 2027.

- PAYE and National Insurance monthly payments are due on the 19th if you pay by bank transfer or cheque, or on the 22nd if you pay by direct debit.

- VAT returns and payments are due one month and seven days after the end of each VAT quarter.

- Corporation tax for most small companies is due nine months and one day after the end of the accounting period.

- Capital gains tax on UK residential property must be reported and paid within 60 days of completion.

Last reviewed: April 2026. All deadlines on this hub reflect the 2026/27 tax year (6 April 2026 to 5 April 2027).

Introduction: The UK Tax Year 2026/27 at a Glance

The UK tax year sets the dates for when income is assessed and when taxes are due for individuals, employers, and companies. Every filing and payment obligation falls on fixed HMRC dates. These dates do not change unless HMRC issues formal extensions.

This calendar brings together every major HMRC deadline for the 2026/27 tax year. It follows current HMRC deadlines 2026 2027 and ICAEW guidance. This hub is for UK accounting practices that need a reliable reference to send to clients. It also serves SME owners and sole traders managing their own HMRC deadlines, finance leads at small and mid-size businesses, and individuals tracking Self Assessment and PAYE deadlines.

From our work at Acenteus Accounting supporting UK firms and SMEs, we see clients miss deadlines most often because they do not know when taxes are due across all their obligations. This calendar removes that uncertainty by listing every key date in one place.

What Are the UK Tax Year Start and End Dates?

The UK tax year does not follow the calendar year.

- Tax year start date: 6 April 2026

- Tax year end date: 5 April 2027

These tax year dates apply to income tax reporting for individuals and partnerships. They also determine the basis for Self Assessment and PAYE reporting cycles.

The structure remains consistent with HMRC’s framework and is reflected in ICAEW technical updates for companies preparing for 2026/27 ICAEW prepare for 2026/27 (businesses). The 2026/27 tax year end date is therefore 5 April 2027.

When clients ask when the UK tax year starts and ends in 2026, the clear answer is 6 April 2026 to 5 April 2027. This is the same every year and does not change.

These tax year dates form the backbone of all personal tax planning and compliance. They determine when income is taxed, when personal allowances reset, and when reporting obligations arise.

For sole traders and partners, the tax year defines the basis period for income tax. For employees, it affects how PAYE coding notices are issued and when tax code changes come into effect.

Many firms use outsourcing for accountants to manage client queries around tax year dates during April and January.

Self Assessment Deadlines 2026/27

Self Assessment deadlines are fixed each year and do not move unless HMRC announces an exceptional extension.

| Requirement | Deadline |

|---|---|

| Register for Self Assessment (new taxpayers) | 5 October 2026 |

| Paper tax return submission | 31 October 2026 |

| Online tax return submission | 31 January 2027 |

| Balancing payment | 31 January 2027 |

| First payment on account | 31 January 2027 |

| Second payment on account | 31 July 2027 |

All dates align with HMRC guidance on Self Assessment deadlines. Payment obligations follow HMRC rules for paying your Self Assessment tax bill.

The self assessment deadline UK 2027 for online filing is 31 January 2027. This is also when the balancing payment and first payment on account are due.

The tax return deadline in the UK for online filing is 31 January. Paper returns must be submitted by 31 October to avoid having to file online.

New taxpayers who became self-employed in the 2025/26 tax year must register for Self Assessment by 5 October 2026. This gives HMRC time to issue a UTR and activate the online account before the filing deadline.

Payments on account are advance payments towards the next tax bill. Each payment is 50 per cent of the previous year’s tax liability, unless the taxpayer qualifies for an exemption.

When clients ask what the self assessment deadline is for 2026/27, the key date is 31 January 2027 for online returns and payment. For paper returns, the deadline is 31 October 2026.

When clients ask when the tax return deadline is in the UK, the answer for online filing is 31 January 2027. This is the date most individuals and sole traders need to remember.

During January, firms typically experience pressure across filing teams. This is especially true when client volumes are high and internal resources are stretched, as outlined in the peak season playbook.

Many accounting practices outsource tax compliance to manage peak workload without overstaffing permanently.

Where readers want planning guidance alongside dates, they can follow year-end tax planning steps to reduce late-filing risk.

When clients ask when taxes are due for Self Assessment, the main answer is 31 January for online filing and payment. Secondary dates are 31 October for paper returns and 5 October for registration.

What happens if you miss the self assessment deadline? The immediate penalty is £100, even if no tax is owed. Further penalties escalate after three months and six months.

PAYE and Payroll Deadlines 2026/27

PAYE operates on real-time reporting, supported by fixed annual submissions.

| Requirement | Deadline |

|---|---|

| FPS (RTI submission) | On or before each payday |

| Final FPS for 2025/26 | 19 April 2026 |

| P60 issued to employees | 31 May 2026 |

| P11D submission to HMRC | 6 July 2026 |

| P11D issued to employees | 6 July 2026 |

| Class 1A NIC (cheque) | 19 July 2026 |

| Class 1A NIC (electronic) | 22 July 2026 |

| Monthly PAYE/NIC (non-direct debit) | 19th of each month |

| Monthly PAYE/NIC (direct debit) | 22nd of each month |

| Mandatory payrolling of benefits in kind | Fully mandatory from 6 April 2026 |

Payroll reporting obligations are set out in HMRC payroll annual reporting requirements. The P60 deadline UK 2026 requires employers to provide forms by 31 May, as confirmed in HMRC P60 guidance.

The P11D deadline in 2026 is 6 July for both submission and employee copies. Supporting rules are set out in HMRC expenses and benefits guidance.

From 6 April 2026, payrolling of benefits in kind is mandatory. Reporting moves into payroll systems rather than year-end forms.

Monthly PAYE liabilities remain due on the 19th or 22nd depending on payment method. This is the answer to when PAYE payments are due to HMRC each month.

The payroll year end deadline UK 2026 is 19 April for the final FPS submission for the 2025/26 tax year.

When clients ask what the P60 deadline is for 2026, the answer is 31 May 2026. Employers must issue P60s to all employees by this date.

When clients ask when the P11D deadline is in 2026, the answer is 6 July 2026 for both submission to HMRC and issuing copies to employees.

Many firms now rely on cloud-based payroll processing aligned with Xero and QuickBooks integrations.

Where payroll volumes increase, especially across multi-client environments, firms often extend capacity using cloud-based payroll outsourcing and maintain compliance with UK payroll requirements for 2026.

Accounting practices often outsource payroll to reduce administrative burden during busy periods.

VAT Return and Payment Deadlines 2026/27

VAT operates on quarterly reporting cycles unless the business uses an alternative scheme such as annual accounting.

- VAT return deadline UK 2026: One month and seven days after the end of the VAT quarter

- VAT payment deadline: Same as the return deadline

All obligations follow HMRC VAT payment rules.

Businesses using the annual accounting scheme must file within two months of the end of their VAT accounting period.

The VAT registration threshold is £90,000 taxable turnover in a 12-month period. This is set out in official VAT guidance on .UK.

In practice, firms handling multiple VAT clients often centralise workflows through VAT compliance outsourcing to manage deadlines consistently.

When clients ask what the VAT return deadline is for UK businesses, the answer is one month and seven days after the end of each VAT quarter.

UK small businesses with multiple VAT quarters must track each quarter end carefully to avoid missing the VAT return deadline UK 2026. This is one of the key HMRC deadlines for UK small businesses in 2026/27.

Corporation Tax Deadlines 2026/27

Corporation tax deadlines depend on the company’s accounting period rather than the tax year.

| Requirement | Deadline |

|---|---|

| Corporation tax payment (small companies) | 9 months and 1 day after period end |

| Quarterly instalments (large companies) | From month 7 of accounting period |

| CT600 filing deadline | 12 months after period end |

These deadlines are set out in HMRC corporation tax rules.

The corporation tax deadline UK 2026 for payment typically falls before the filing deadline. Companies must pay before submitting their CT600 return.

For small companies, corporation tax is due nine months and one day after the end of the accounting period. This is the answer to what the corporation tax payment deadline is for UK companies.

Large companies pay through quarterly instalments starting from month seven of the accounting period. This applies to companies with profits above the upper limit for instalment payments.

ICAEW guidance for companies confirms the structure and timing of obligations across accounting periods ICAEW prepare for 2026/27 (companies).

Firms managing high volumes of company accounts often coordinate these deadlines alongside statutory accounts and filings using accounting outsourcing for UK accounting firms.

Many practices use white-label outsourced services to handle corporation tax compliance for their clients.

Capital Gains Tax Deadlines 2026/27

Capital gains tax applies when individuals or businesses dispose of chargeable assets such as property, shares, or business assets.

- CGT on UK residential property: Report and pay within 60 days of completion

- CGT via Self Assessment: 31 January 2027 for disposals in the 2025/26 tax year

These requirements follow HMRC capital gains tax rules.

The capital gains tax deadline UK 2026 for property disposals is strictly enforced. The 60-day reporting window applies from the completion date, not the exchange of contracts.

When clients ask how long they have to report and pay capital gains tax on a property sale, the answer is 60 days from completion for UK residential property.

CGT on other assets such as shares or business assets is reported through Self Assessment by 31 January 2027 for disposals in 2025/26. This aligns with the online tax return deadline.

National Insurance Deadlines 2026/27

National Insurance contributions follow PAYE timelines for employees and Self Assessment timelines for the self-employed.

- Class 1 NIC: Paid monthly alongside PAYE by the 19th or 22nd

- Class 2 and Class 4 NIC: Paid via Self Assessment by 31 January 2027

These deadlines align with HMRC payment structures under Self Assessment and payroll systems.

Employers pay Class 1 NIC at the same time as PAYE, either on the 19th or 22nd depending on payment method. Self-employed individuals pay Class 2 and Class 4 NIC through their Self Assessment bill.

For sole traders, these obligations sit alongside wider Making Tax Digital changes, particularly for those transitioning into quarterly reporting under MTD for Income Tax from April 2026.

MTD compliance solutions help practices manage quarterly reporting for clients moving into Making Tax Digital.

Other Key HMRC and Companies House Deadlines 2026/27

Additional statutory deadlines apply to companies and regulated businesses beyond core tax obligations.

- Confirmation statement: Due annually within 14 days of the review period end, as required by Companies House filing rules

- Annual accounts (private companies): Due 9 months after accounting period end

Making Tax Digital for Income Tax applies from April 2026 to sole traders and landlords earning over £50,000. This is confirmed in HMRC Making Tax Digital roadmap.

Construction businesses must also align with CIS reporting cycles, especially with updates impacting subcontractor reporting obligations under CIS compliance changes for 2026.

Many firms reassess internal delivery models when managing these overlapping deadlines, especially given the accountancy talent shortage and capacity constraints across UK practices as outlined in this analysis.

For SMEs needing ongoing support across multiple obligations, accounting services for small businesses often include outsourced bookkeeping, VAT, payroll, and compliance functions.

Firms considering offshore support often compare offshore and onshore accounting models to balance cost, security, and quality in this comparison.

Security and data protection are critical when outsourcing. Practices should check for GDPR and security red flags before engaging an outsourced accounting provider as set out here.

Accounting outsourcing for UK accounting firms provides a structured way to handle year-end bottlenecks and seasonal peaks.

Firms looking for a clear understanding of outsourced accounting can consult the complete accounts outsourcing UK guide.

Many practices also outsource VAT work to reduce workload without sacrificing quality.

What are the key HMRC deadlines for UK small businesses in 2026/27? The main ones are Self Assessment by 31 January, VAT returns one month and seven days after quarter end, PAYE monthly by the 19th or 22nd, and corporation tax nine months and one day after period end.

What Happens If You Miss an HMRC Deadline?

HMRC applies penalties automatically once deadlines are missed.

- Self Assessment: £100 fixed penalty immediately after 31 January, with further daily penalties after three months

- Late payment: Interest accrues from the due date at HMRC’s statutory rate

- VAT: Default surcharge or penalty regime depending on compliance history and number of defaults

- PAYE: Penalties based on frequency and lateness of submissions, plus potential interest on late payments

Late filing and payment penalties are automatic under HMRC systems. Once triggered, they escalate quickly if not resolved.

When clients ask what happens if you miss the self assessment deadline, the immediate answer is a £100 penalty. Further penalties apply as time passes.

The main risk is often late filing rather than inability to pay. This is particularly true during peak reporting periods where internal workflows are under pressure.

In practice, firms often use outsourcing for accountants to handle extra filing workload without overstaffing permanently.

Firms managing high volumes may also review how outsourcing supports capacity planning as explained in this guide.

Many firms start at the homepage to understand the full range of outsourced accounting and finance services available.

Conclusion: Keep This Page Bookmarked

For ongoing compliance support across filing deadlines and reporting cycles, Acenteus

Frequently Asked Questions (FAQ)

The 2026/27 tax year starts on 6 April 2026 and ends on 5 April 2027. These dates determine how income is assessed and reported for individuals and businesses.

The online filing deadline is 31 January 2027. This is also the final date for submitting returns and paying any outstanding tax for the 2025/26 tax year.

Yes. Paper returns must be submitted by 31 October 2026. After this date, HMRC requires online submission unless specific exemptions apply.

The main payment deadline is 31 January 2027. This includes any balancing payment for the previous tax year plus the first payment on account.

Payments on account are advance payments towards your next tax bill. They are due on 31 January 2027 and 31 July 2027.

Employers must issue P60 forms by 31 May 2026. This summarises total pay and deductions for the previous tax year.

You must register by 5 October 2026 if you started trading in the 2025/26 tax year and need to file a return

A £100 fixed penalty applies immediately after the deadline. Additional daily penalties and interest apply if the delay continues.

Corporation tax is due nine months and one day after the end of the accounting period. The return itself is due 12 months after that period ends.

No, unless you are voluntarily registered for VAT. If registered, you must file returns regardless of turnover level.